Think about how the medical field treats data.

Before a new drug reaches your pharmacy, or a new implant reaches an operating room, somebody had to prove it works. Not with a good story. Not with one doctor’s hunch. With statistics — controlled trials, large sample sizes, results that hold up when other professionals check the math. We demand that level of rigor in medicine for an obvious reason: the stakes are our health.

Now think about how most people treat investing.

Investing isn’t life and death, but the stakes are real. If you make poor investment decisions for thirty years, you don’t find out gradually — you find out at retirement, when you arrive with a lot less than you could have had. There’s no do-over at that point. You’d think a decision with consequences like that would get the medicine treatment: careful analysis, real evidence, conclusions drawn the right way.

Mostly, it doesn’t. People buy an investment because a personality on TV is excited about it, or because it’s what everyone seems to be talking about right now. That’s not analysis. That’s fashion.

A field that flew blind for a long time

Here’s something that surprises people: the U.S. stock market operated for well over a century before anyone systematically measured what it had actually returned. Until the 1960s, if you asked what the long-term return of stocks was, the honest answer was that nobody knew — people were guessing. It took an enormous academic effort to assemble the data and find out. Dimensional’s David Booth tells the story of that project, called CRSP, in a piece we recently shared on our blog, and it’s worth a read — it’s the moment investing started becoming something you could study instead of something you could only argue about.

Why investing needs statistics more than most things

Investment returns are noisy. Really noisy. A fund can beat the market three years running on pure luck, and a sound strategy can trail the market for stretches long enough to test anyone’s patience. When data is that noisy, statistics gives you a clear instruction: you need a much larger sample before you conclude anything. One hot year tells you almost nothing. Even five years tells you less than you’d think.

That’s exactly backwards from how the headlines work, which celebrate last year’s winner as if one year settles the question.

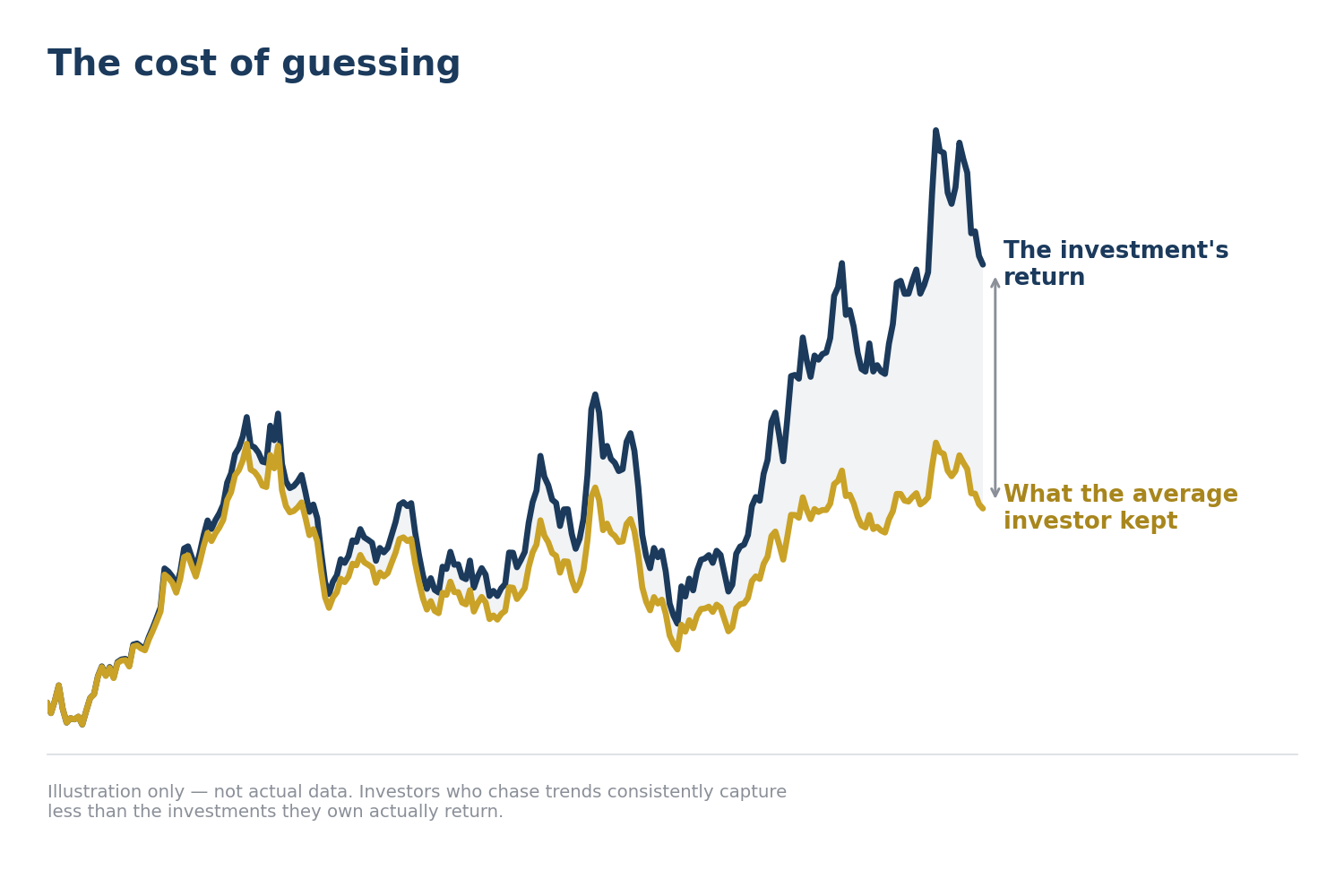

What guessing actually costs

This isn’t hypothetical. Two long-running studies — Morningstar’s “Mind the Gap” and DALBAR’s Quantitative Analysis of Investor Behavior — have been comparing the returns funds earn to the returns their investors actually receive, year after year, for decades.¹ The studies use different methods and the size of the gap varies depending on how and when you measure it, but the direction never changes: investors as a group consistently capture less than the return that was sitting right there waiting for them. The cause is timing — buying after things went up, selling after things went down.

The extreme version of this story is famous. The single best-performing U.S. stock mutual fund of the 2000s returned about 18% per year — over a decade when the broad market went roughly nowhere. Its typical investor lost about 11% per year.² Same fund. The fund did its job; the investors poured in right after the spectacular years and bailed right after the painful one. Owning the right thing isn’t enough if you can’t stay in your seat.

Illustration Only - Not Actual Data

The standard your money deserves

You wouldn’t take a medication because your neighbor swears by it. You’d want to know it had been tested — properly, statistically, on more than a handful of people. Your retirement deserves the same standard: decisions based on statistically validated evidence, drawn from the largest samples available, held long enough for the evidence to work.

That’s what evidence-based investing means to us at O’Reilly Wealth Advisors, and it’s why we build portfolios with Dimensional Fund Advisors, a firm whose entire approach grew out of that same rigorous returns data. It doesn’t make investing exciting. It makes it dependable. For something you only get one shot at, dependable wins.

Footnotes

¹ Morningstar, “Mind the Gap 2025” (dollar-weighted investor returns vs. total returns of U.S. mutual funds and ETFs); DALBAR, “Quantitative Analysis of Investor Behavior,” published annually since 1994.

² Morningstar investor-return data on the CGM Focus Fund, ten years ending November 30, 2009, as reported in The Wall Street Journal (“Best Stock Fund of the Decade,” December 2009). Historical example for educational purposes only.

This article is for educational and informational purposes only and does not constitute investment, tax, or legal advice, nor a recommendation to buy or sell any security or to adopt any investment strategy. All investing involves risk, including the possible loss of principal, and past performance is not a guarantee of future results. Please consult a qualified professional regarding your individual circumstances before making any financial decisions.